Analysis in brief: Financial technologies (Fintech), most notably doing banking tasks using a smartphone app, have become a way of life for many Africans, clearly showing the future of African financial services. While traditional banks are offering mobile apps of their own, they are also embracing Fintech start-up firms run by savvy young entrepreneurs bringing new ideas.

From pandemic life-saver to post-pandemic financial essential

The Covid-19 pandemic devastated African economies, while at the same time forever reshaping these economies by accelerating the way Africans conduct business. Confined to their homes, some Africans could still order items at online stores and restaurants for residential delivery, pay bills and transfer money. Post-pandemic, as the number of smartphones increased (in some countries, surpassing the number of people), online apps enabled a diversity of financial services. The Fintech that created these instantaneous services, which lessened the destructiveness of the Covid pandemic by enabling financial transactions online, have shown the way forward for the financial industry.

In one sense, Fintech services are revolutionary (in the business world, the word is “disruptive,” such as “financial apps are disrupting – e.g., displacing – traditional banking services.”). However, in another way, Fintech services have come to augment rather than replace traditional banking services. Banking customers do not yet enjoy online savings accounts that are insured by any country, and to them, obtaining a loan online is a risky affair. The lack of such online financial services may be resolved through national regulations of Fintech.

There are no continental regulations. It would be relevant if the African Union as the only body in the position to promulgate such regulations, would take up the issue. National regulations vary from country to country, making business difficult for Fintech companies seeking to operate continentally. Meanwhile, traditional banks, which do operate in an established regulatory environment, are expanding their Fintech offerings however they can. This has meant that national regulatory mechanisms have had to make new rules for the use of Fintech for banks. These regulations can become applicable to Fintech firms that operate using smartphone apps. The largest of these in Africa are Fawry, M-Pesa and OPay. The three firms will expand significantly in their continental reach once regulations pave the way. Meanwhile, while investment in Fintech start-ups remains robust, it has slowed since the pandemic crisis ended, when Fintech rode to the rescue of home-bound consumers.

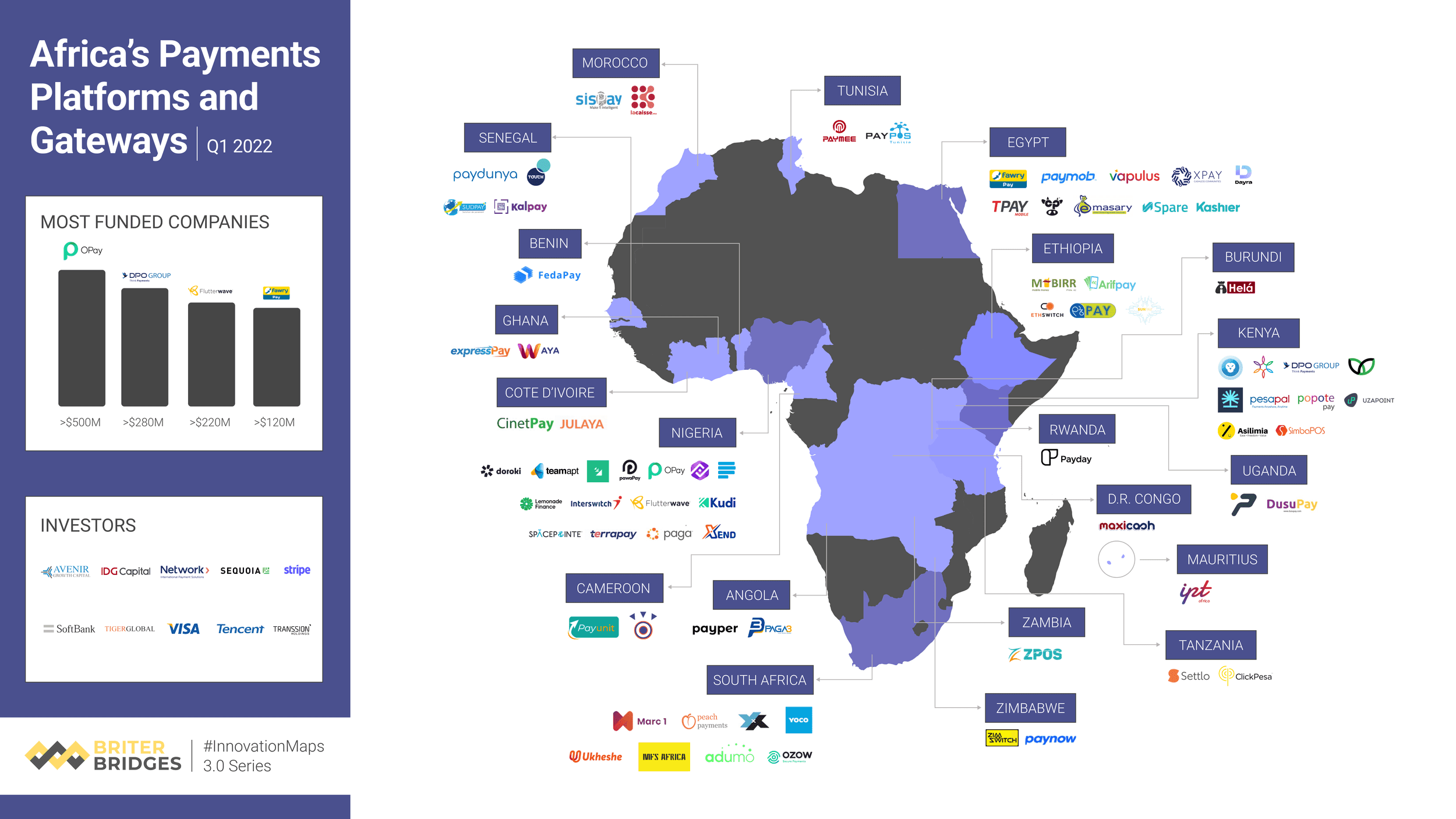

Data courtesy: Briter

Room for Fintech growth

African consumers have thoroughly embraced their smartphones, using these devices for telephonic communication, photo taking, video and voice recording, entertainment, news, weather reports, study and research, gaming and all manner of internet-based activities. The growth of Fintech is tied to the smartphone boom and is limited only by the degree that cellular and satellite technology keeps apace and then keeps ahead of demand. Data costs are another encumbrance to the use of Fintech, although data costs also tend to be cheaper than fees charged by banks for financial transactions.

It is not reliably known how many Africans do not have access to banking services. In South Africa, which is Africa’s third largest economy, about 24% of the population are not bank customers. However, continentally over the past decade, the number of Africans who have opened bank accounts has increased by 20%, according to Oxford Business Group. These customers will likely be introduced to banking online through their bank’s own apps. This will lead to making use of other apps for financial services, online purchases and money transfers beyond the capabilities of what their local banking apps can offer.

One challenge faced by Fintech apps is the lag time for money transfers, particularly from one bank to another. Only three African countries currently have real-time payment, whereby the receiver is instantly credited with the money originating from the sender’s end.

Perhaps the greatest reason for African Fintech start-up companies to seek investment financing from their local banks and to embrace such investment when offered is the security of dealing with a partner that is a mutual beneficiary of their country’s economic growth. Currently, 70% of investment for Africa’s Fintech start-ups comes from outside Africa, particularly from North America. International investment trends are constantly shifting, and foreign investors have different priorities to local ones. The African Development Bank (AfDB) recognises this reality. On 26 April 2023, AfDB extended a US$ 525,000 grant to Nigeria’s Africa Fintech Network to help finance the Africa Fintech Hub that aims to boost the continent’s capacity to provide all Africans with digital financial services.

President of Africa Fintech Network, officiate as the AfDB extends the grant for Africa’s Fintech development

Image courtesy: Government of Ghana

Conclusion:

While communications infrastructure is extended into currently underserved areas, urban migration is bringing a steady stream of new customers of Fintech services to urban areas. Here, they can employ smartphone apps for financial services that most Africans could never access before. While international firms like Visa are investing in Africa’s Fintech start-up companies, perhaps the most important investors are African banks. The Big Five banks, including FNB and Standard Bank, are already invigorating their financial services practices through such investments, making it industry practice.

The critical points:

- Proving its value during the Covid-19 pandemic by bringing retail and financial services to home-bound consumers, Fintech has become a way of life for a growing number of Africans

- African banks and African Fintech start-ups are natural partners, and more local investment will bring stability to a start-up industry dominated by overseas investors

- Government regulation of Fintech and the expansion of cellular infrastructure are a prerequisite to universal use of Fintech by Africans