Analysis in brief: The varying degrees of economic growth between Africa’s five regions illustrates how fundamentals like electricity supply determine economic performance. Continentally, Africa is achieving good – if delayed – post-Covid epidemic growth.

Overall, Sub-Saharan Africa will record positive economic growth in 2024, according to the African Development Bank and the World Bank, although the forecast degrees vary. However, for some countries, even positive growth is insufficient if it falls below population growth, leading to new jobs being created for an unmatched number of job seekers. True economic growth must raise the standard of living for all the citizens of a country. This cannot be achieved when economic inequity results from a country’s elite controlling a large percentage of a country’s wealth, leaving the large majority of the population mired in poverty. While economic inequity must be addressed as an ongoing concern, this paper’s focus is on the rising countries’ economic performances.

In 2024, Sub-Saharan African national economies are performing under their governments’ adherence to basic economic necessities and trade rules. They underperform when the same necessities are lacking. When infrastructure is problematic, even the most powerful economies suffer. Countries in Northern Africa that rely on the export of raw commodities continue to have their economic fortunes held hostage by fluctuating global commodity prices. Their failures to diversify economies from a single revenue source holds back their economic growth and national development. Conversely, Sub-Saharan African countries that observe these economic realities are doing relatively well.

Africa’s worst-performing sub-region is hindered by unique national challenges

Of Africa’s five sub-regions, Southern Africa performed demonstrably worse in 2023. Growth of 1.3% was about a third of West Africa’s 3.2%, East Africa’s 3.5% and Central Africa’s 3.8%. This is because of the poor performance of powerful economies whose declining fortunes dragged down the entire sub-region, whose lesser economies are systemically tied to their neighbouring developmental giants. In Southern Africa, Angola and South Africa were these anchors, dragging down the sub-region, much as they buoy Southern Africa economically during the years when their economies perform well. The situation is similar to what happened in Nigeria in 2023. The country’s economic decline affected the entire West African sub-region, making it one of the worst performer in Sub-Saharan Africa outside Southern Africa.

The economic decline of Angola, Nigeria and South Africa is due to factors unique to those countries, but these can be addressed through economic policies and infrastructure investment. Economists suggest that all these countries suffered from post-Covid epidemic effects of global recession coupled with the inflationary pressures from the necessities of oil and food. Yet, a closer look finds each country is economically governed by its own fixable problems. Angola, despite being Africa’s largest oil exporter, faces the challenge of aging oil fields that have been the primary source of revenue for its oil-dependent economy, used to finance national development. The solution is clear, that of economic diversification into other income generating streams like value-added industry. The country has seen some movement in this direction in government policy and investment. Equally clear is that more policy innovation and private investment are needed; however, Luanda appears to know what it must do in terms of policies and incentives. Similarly, South Africa’s energy crisis, which has eroded industrial output, slashed worker productivity and left a population struggling with blackouts, knows what it must do: invest in electricity production.

The Mauritius model offers guidance

Botswana and Rwanda, the only two Sub-Saharan African economies to see double-digit growth in 2021, saw this growth radically drop in subsequent years: Botswana dropped from 11.8% in 2021 to 3.8% in 2023 and Rwanda from 10.7% in 2021 to 3.6% in 2023. Zimbabwe’s robust 8.5% growth in 2021 and Kenya’s 7.6% growth that year dropped to 4.5% and 5% respectively in 2023. By contrast, Mauritius’s 2021 GDP growth of 3.4% rose to 5% in 2023. The return of tourism post-Covid had an effect – neighbouring Comoros also saw GDP rise from 2.1% to 3% from 2021 to 2023 due partly to tourism – but the primary factor was the continuous success of Mauritius’s long-term effort to position itself as an off-shore financial centre, which has drawn business from India in particular. Of the other Indian Ocean nations, Tanzania saw its GDP grow comfortably from 4.3% in 2021 to 5.1% in 2023 as its own financial sector became the recipient of government policy attention and international investment, expanding to rival East Africa’s financial capital, Nairobi, Kenya. The lesson is that economic diversification from commodities like minerals and agricultural products towards services that can be purchased by foreigners, such as equities on a local stock exchange or tourism opportunities, drive economic growth if forward-thinking governments can embrace new revenue streams.

Mauritius is also a politically stable and peaceful country, with both factors influencing foreign investors’ interest in any country. Africa offered other examples of this in 2023. When mineral prices were depressed globally, the Democratic Republic of Congo, whose economy principally relies on mineral exports, saw a bump in GDP growth from 2021 to 2023 (6.2% to 6.8%) because the perennial conflict that has long plagued the mining sector became less volatile. Similarly, when all of Sub-Saharan African countries experienced economic declines post-Covid, Guinea experienced decent growth from 4.3% in 2021 to 5% in 2023 due to improved national security and government stability, as reflected in investors’ surveys.

Image courtesy: Central Bank of Mauritius

Daunting challenges despite upward growth

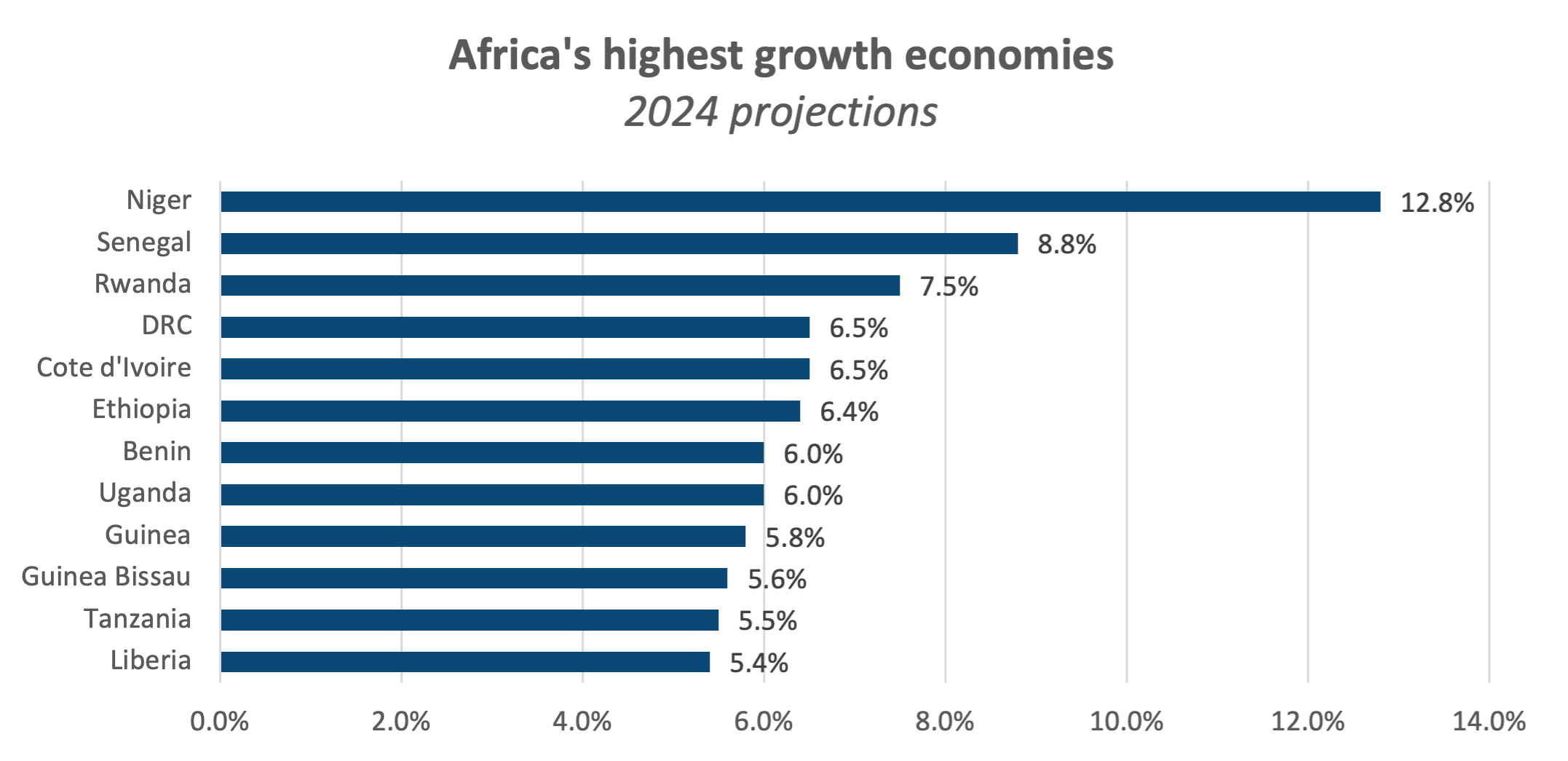

Altogether, 15 African countries had GDP growth higher than 5% in 2023. The African Development Bank reports that, in 2024, Africa will account for 11 of the world’s 20 fastest-growing economies. Africa’s overall real GDP growth is forecast to average 3.8% and 4.2% in 2024 and 2025, respectively. By comparison, projected global economic growth will be 2.9% in 2024 and 3.2% in 2025. In terms of rapidity, Africa will be the second-fastest-growing region after Asia. The top 11 African countries projected to experience strong economic performance forecast are Niger (11.2%), Senegal (8.2%), Libya (7.9%), Rwanda (7.2%), Cote d’Ivoire (6.8%), Ethiopia (6.7%), Benin (6.4%), Djibouti (6.2%), Tanzania (6.1%) and Togo and Uganda (tied at 6%).

Two factors account for these upward trends: Africa is rising from a low economic base, which gives even small investments oversized impact on GDP numbers, and Africa has lagged behind the world in post-Covid pandemic recovery and is only now gaining ground. On the whole, Africa’s economies have lost years of growth because of the pandemic, and in most cases, national economic output has not returned to 2019 levels. Furthermore, Africa faces economic hardships from climate change more severely than other world regions. However, African governmental policies are becoming more responsible for debt management – the African national debt of 4.9% in 2023 is significantly less than the 6.9% in 2019 – and economic policies increasingly favour economic diversification and value-added production, known as resource-based industrialisation. These developments will better enable African countries to weather global economic shocks like global commodity price fluctuations in the future.

The critical points:

- Africa is the world’s second fastest growing region economically, but this is due to late recovery from the Covid pandemic

- Poor performance from major Sub-Saharan African economies negatively affects entire sub-regions

- Governmental economic policies improving national debts and boosting economic diversification coupled with investment in value-added manufacturing are key to GDP growth