Analysis in brief: African countries are consistently targeted by terrorist organisations, but nearly two-dozen governments are failing to follow international guidelines to stop the financing of these groups. Harm to national economies results, while an unintended failing of governments, is a beneficial outcome for terrorists seeking to destabilise Africa.

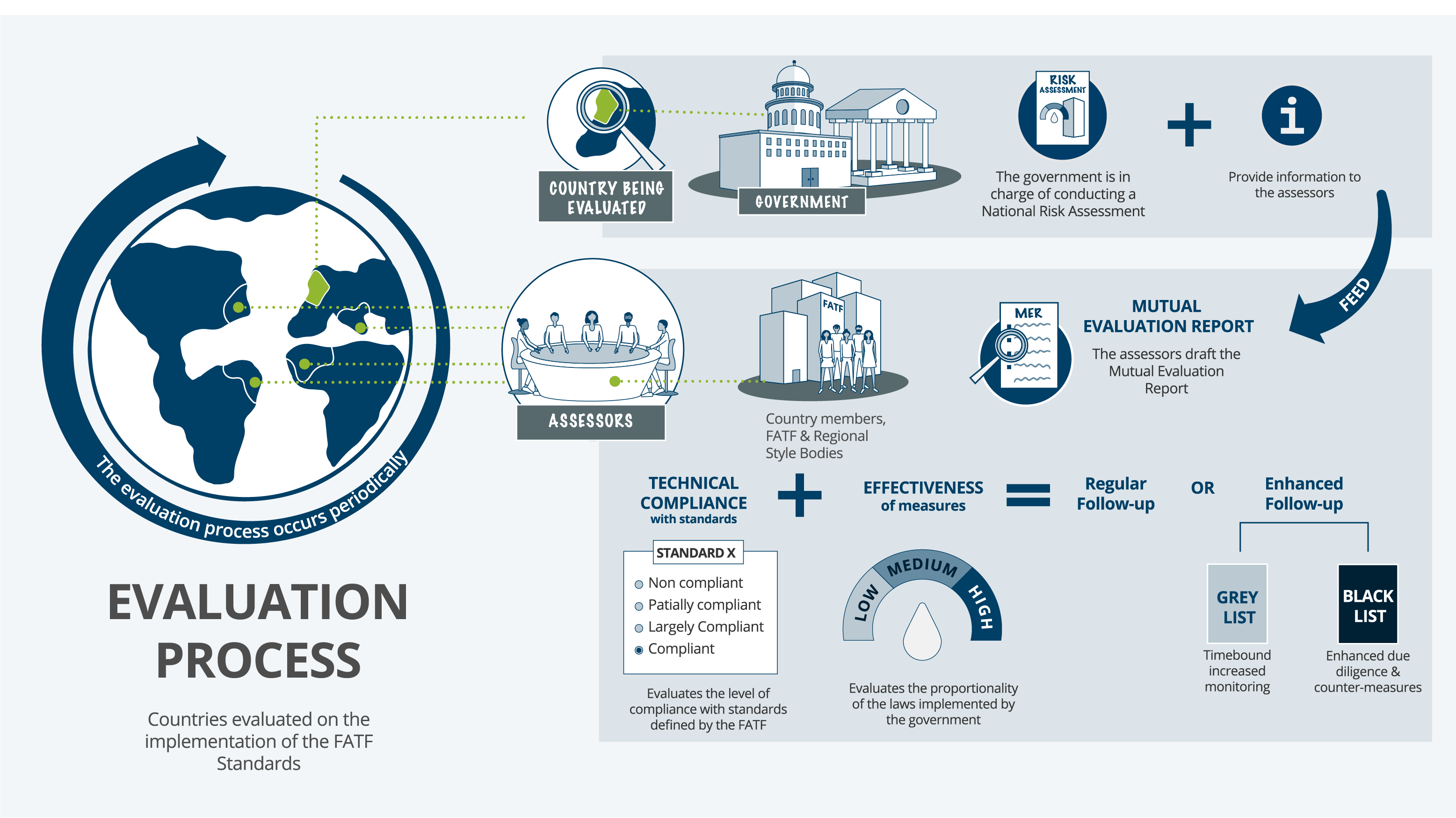

The Financial Action Task Force (FATF) is the international community’s answer to terrorist financing. FATF sets guidelines for governments to stem the flow of money to terror groups and steers countries towards meeting those goals. However, achieving regulatory reform can be one cost too many for poor African countries. Consequently, half (12 of 21) of the countries ‘greylisted’ by FATF are African. Blacklisted countries like Iran and North Korea are actual sponsors of terrorism: These are sovereign states where funding originates, which is then distributed across Africa through a system of corrupt politicians, crooked accountants, underhanded lawyers and lackadaisical banks with money transfer oversight. Countries that allow this to happen become facilitators of terrorism and are greylisted for this authorisation. To return to legitimacy, they need to clean up their acts by enacting financial reform measures. In addition, to demonstrate their serious intentions, governments need to prosecute money launderers.

| African countries on FATF’s greylist | |

| Countries | Greylisted since |

| Burkina Faso | Feb 2021 |

| Cameroon | Jun 2023 |

| Democratic Republic of Congo | Oct 2022 |

| Kenya | Feb 2024 |

| Mali | Oct 2021 |

| Mozambique | Oct 2022 |

| Namibia | Feb 2024 |

| Nigeria | Feb 2023 |

| Senegal | Feb 2021 |

| South Africa | Feb 2023 |

| South Sudan | Jun 2021 |

| Tanzania | Oct 2022 |

Source: The Financial Action Task Force

The economic need to be FATF compliant

Whenever the subject of greylisting African countries arises, the argument is raised that the limited national funds must be prioritised for basic services. However, corruption is at the heart of terrorism financing. Corrupt officials do not want FATF compliance because it would interfere with their own illicit earnings made by looking the other way or actively facilitating money laundering and transfers. Such corrupt officials do not prioritise the needs of the populations that they ostensibly serve. This makes specious the argument that cost is the deterrence to drafting regulations and enacting these through police work, prosecutions and banking procedures.

The argument that an indigent country cannot afford FATF compliance is also counter by the encumbrances to national prosperity encountered by countries that do not comply. The international community sees inclusion on the greylist as a warning sign that a country is financially untrustworthy. Foreign investors become wary of doing business in a country with a poorly regulated banking industry. Their hesitancy to invest impacts their countries’ GDP. International aid to a greylisted country becomes problematic. Remittances from abroad take longer to reach their intended recipients. Foreign currency exchange becomes difficult. Banks face higher administrative costs for international transactions, and these are passed on to customers. Half of Sub-Saharan Africans do not have bank accounts, and higher banking fees discourage potential bank customers from opening accounts, while those individuals who do open bank accounts struggle to do so. Instead, people use their smart phones to put their money into risky crypto currencies and make use of digital financial services, both of which are unregulated by African governments. Because most of these governments are also committed to the financial inclusion of their citizenry, they respect public interest and seek to become FATF compliant. Critics of FATF note that compliance requires banks to do more stringent due diligence on customers’ opening accounts, and this raises fees that works against the financial inclusion of the citizenry. However, this expenditure is the elimination of the costs and penalties resulting from non-compliance. Benefits include a stronger, safer economy that draws investors, international aid and respect to a financially responsible country.

FATF insists its role is to guide countries toward financial reforms that will shut down the money flow to terror groups by using a ‘carrot and stick’ approach. The stick is listing a country for non-compliance. The carrot is assistance towards compliance.

Source: Global NPO Coalition on FATF

No common denominator for greylisted African countries

The twelve FATF greylisted countries are large and small, peaceful or torn by conflict, prosperous or impoverished. As East Africa’s financial hub, Kenya cannot afford its inclusion on the greylist. Security is the essential requirement for any nation to become compliant, so South Sudan’s ongoing civil war that undermines governance prevents any possibility that financial regulation can be achieved. Two of Africa’s largest economies are greylisted, Nigeria and South Africa. It is in the best interest of Nigeria’s security to become FATF compliant. Nigeria has been plagued by the local Boko Haram terror group for decades yet cannot stem the financial inflows that enable the terrorists’ activities.

By contrast, South Africa’s government feels it faces no imminent terror danger and lacks the political will to pursue compliance, despite Southern Africa’s first terrorist incursion unfolding in neighbouring Mozambique. Press reports on terrorist training camps set up within South Africa itself, allegedly with the knowledge of government, raises questions on government’s interest in the terrorism issue. South Africa’s opposition parties claim that high-level corruption is the reason for FATF non-compliance. As evidence, they point to incidents of ‘state capture’ – defined by the use of public companies and institutions for the personal gain of powerful and well-connected individuals – and the degradation of police and prosecutorial resources. Indeed, as a member of the BRICS economic block, along with Russia and China, South Africa is considering discarding the current international financial system in favour of a non-dollar and non-Western system. However, whatever economic benefit this may or may not bring, it has nothing to do with the agenda of FATF, which is to stop money laundering and the financing of terror groups. South Africa was greylisted in February 2023; and given the tepid commitment to reform – unlike Nigeria, which is moving ahead to become compliant – two to three years may elapse before compliance is achieved.

The judiciary is also a key player in FATF compliance. Courts must be uncorrupted, and governments’ commitment to upholding laws must be manifested in actual prosecutions. One means for a country to prove it is sincere in its aim to be FATF compliant is to prosecute money launderers and enact such measures as confiscation of fraudulent finances and the sanctioning of individuals. South Africa has been alerted to money launderers residing within its borders but has taken no action.

Reform is possible where there is political will

Being greylisted is a reputational blow to any country and should be a source of embarrassment for national leaders. This may be what ultimately prompts South Africa to increase the pace of financial reforms that have already begun. The first step for any greylisted country to be removed from the list is to draw up an action plan that shows the remedial steps to address systemic vulnerabilities that allow money laundering and other means of terrorism financing to flourish. The action plan is submitted for approval by FATF, which offers technical assistance to achieve the plan’s goals. Technical support is also forthcoming from the European Union, the International Monetary Fund and the World Bank, as well as the UK and the US.

Being on the FATF greylist creates such onerous effects for a country’s economy that some African countries have proven that they are indeed interested in their citizens’ financial welfare. After taking action, these countries have been dropped from the list. It can be done. Botswana, Mauritius, Morocco and Zimbabwe are all examples of this possibility, and all these countries, except for Zimbabwe, now have robust economies.

There are specific measures required of governments that invariably appear in these action plans (See side-box). Kenya and Namibia are at an advanced stage toward achieving these measures. FATF notes that both these countries enjoy “high-level commitment” towards financial reform. Conversely, South Africa’s president has not demonstrated leadership in this matter. As a result, the national treasury has complained that there is only so much it can do to confront a dilemma that requires a multi-sector solution, and that while the treasury can do its part, it has no control over the police, public prosecutor, the business sector and even the civil sector – all of whom have roles to play in achieving compliance. Only the presidency can bring together such disparate governmental and national players.

Source: The Financial Action Task Force

The critical points:

- More than half of the world’s countries that are greylisted for failing to stop money from reaching terrorist groups are African

- Political leadership from a nation’s top authority is required to stop money laundering and other illicit financial acts that benefit terrorists

- Micro- and macro-consequences befall countries that are blacklisted – from lower GDP growth to difficulties of their citizenry and companies attempting financial transactions